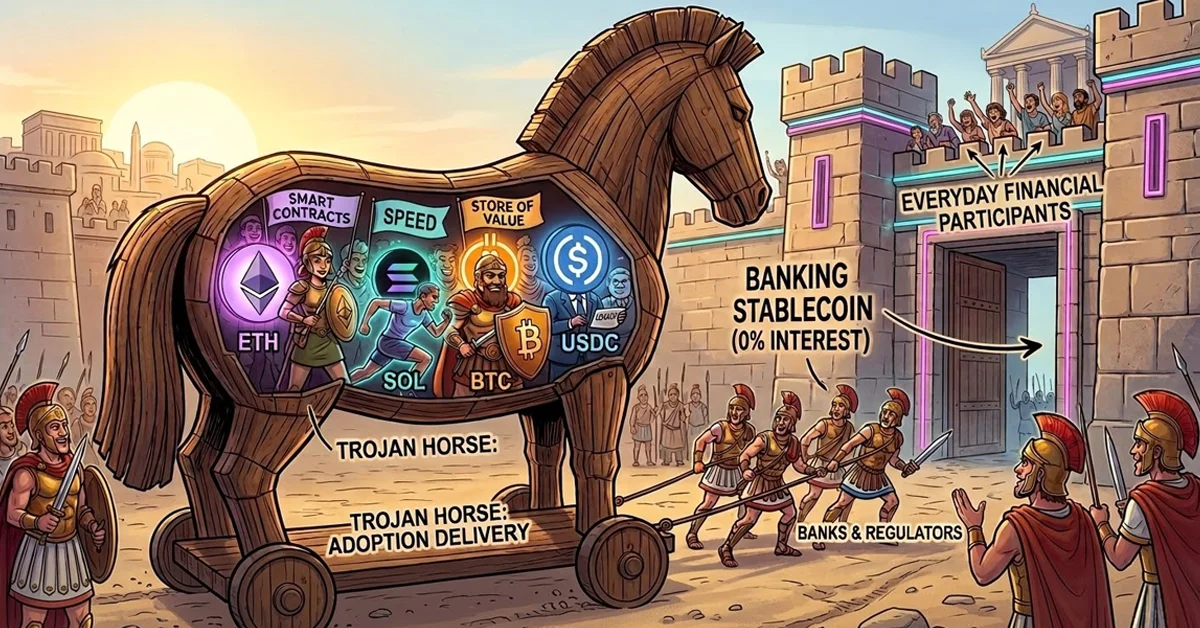

The passage of the Interest-Free Trojan Horse dynamic began with the GENIUS Act in July 2025, which marked a new chapter for the American financial system by giving banks a clear path to adopt digital assets. By early 2026, the total value of stablecoins has climbed to more than $300 billion. These tokens are digital assets designed to stay worth exactly one dollar and are usually backed one to one by safe reserves such as cash or short-term government bonds. This design is what finally convinced traditional banks to stop fighting the blockchain and start building on it. This shift is crucial because it aligns the goals of legacy finance with the growth of the crypto industry.

If stablecoins offered high interest, they would drain the cash that people keep in their local bank accounts. This would create a conflict between new technology and the banks that fund our communities. Research from early 2026 shows that when digital assets compete for deposits, it can create unwanted stress on the banking sector. By keeping stablecoins interest free, the crypto industry can grow without breaking the foundation of the economy. This makes it easier for banks to move their customers onto the blockchain safely because it does not threaten their core business of holding deposits.

Tokenized Deposits and the Bank Incentive

The real benefit appears when examining how banks use these funds through tokenized deposits. In this model, the stablecoin acts like a digital receipt for a dollar held at the bank. While that digital token circulates in payments or Web3 applications, the bank still holds the actual reserve. This allows the bank to continue its normal activities, such as investing those reserves into safe government bonds to earn a profit. Because banks can generate more revenue by managing these reserves than they often do from standard loans, they are increasingly motivated to bring more dollars onto the blockchain. This Interest-Free Trojan Horse model quietly expands blockchain participation while maintaining the traditional banking framework.

Private Stablecoins vs. Government Digital Currencies

This profit incentive is a key reason private stablecoins and tokenized deposits are gaining traction over government-run digital currencies. Regulators in 2026 have signaled a preference for private innovation over a central bank digital currency, or CBDC, that could raise concerns about government overreach. While some governments remain in testing phases, the private sector is already moving trillions of dollars with transparent blockchain systems. These tokenized deposits allow banks to operate under the same safety standards used for decades while delivering the speed and efficiency of blockchain technology. The Interest-Free Trojan Horse approach effectively positions banks as strong participants in the crypto ecosystem rather than opponents.

A Partnership That Drives Blockchain Adoption

Ultimately, the decision to keep stablecoins interest free has created a powerful partnership. It transforms traditional banks from passive observers into primary engines of crypto growth. We are seeing a financial landscape where local banks provide the digital wallets and infrastructure needed to access Web3 systems. By ensuring banks remain profitable during this transition, the Interest-Free Trojan Horse model builds a foundation that could support digital finance for decades. This approach may help ensure that the future of money is secure, widely accessible, and built on technology that can support large-scale liquidity across the blockchain ecosystem.

Disclosures: This article is for informational purposes only and should not be considered financial, legal, tax, or investment advice. It provides general information on cryptocurrency without accounting for individual circumstances. Sarson Funds, Inc. does not offer legal, tax, or accounting advice. Readers should consult qualified professionals before making any financial decisions. Cryptocurrency investments are volatile and carry significant risk, including potential loss of principal. Past performance is not indicative of future results. The views expressed are those of the author and do not necessarily reflect those of Sarson Funds, Inc. By using this information, you agree that Sarson Funds, Inc. is not liable for any losses or damages resulting from its use.