The RWA payments shift is accelerating as stablecoins transition from passive yield instruments into core financial infrastructure. Real-world assets (RWAs), which refer to traditional financial instruments such as dollars, Treasuries, and credit represented on blockchain networks, are increasingly being integrated into modern payment systems.

For years, the primary appeal of stablecoins was the ability to earn interest simply by holding digital dollars. That model changed with the passage of the GENIUS Act in late 2025 and subsequent regulatory guidance from the Office of the Comptroller of the Currency in early 2026, which prohibited issuers from offering interest on holdings.

Rather than slowing adoption, this shift has redirected value creation toward utility. Stablecoins are now used for payments, settlement, and liquidity management. Enterprises are beginning to treat them as operational cash equivalents for cross-border treasury and programmable financial flows.

In several high-friction corridors, stablecoins are already outperforming traditional remittance systems in both cost and speed. They are no longer a destination for capital. They are becoming the infrastructure that enables it to move.

Mastercard’s $1.8 Billion Bridge: The BVNK Acquisition

Mastercard’s $1.8 billion acquisition of BVNK highlights how traditional financial institutions are adapting. BVNK enables seamless movement between fiat currencies and stablecoins across more than 130 countries.

Rather than replacing traditional systems, Mastercard is positioning its network to support multiple forms of digital value, including stablecoins, tokenized deposits, and central bank digital currencies.

At the same time, banks such as JPMorgan Chase and Citigroup are advancing tokenized deposit systems, introducing competition over which form of digital money will dominate settlement.

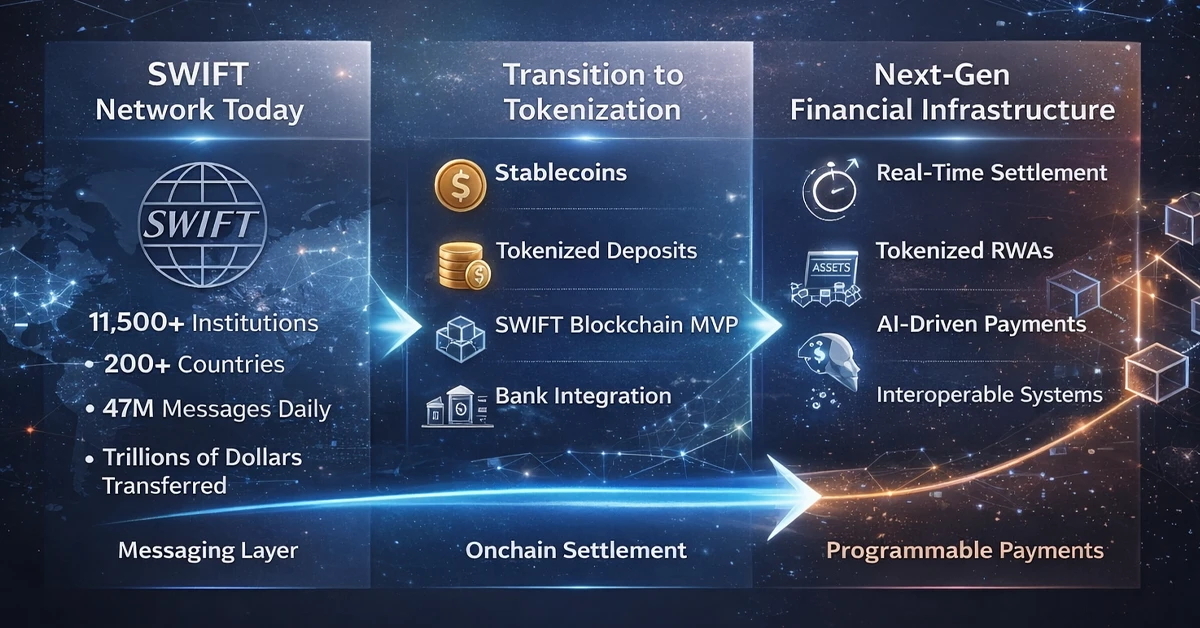

Even SWIFT is moving blockchain-based settlement into a minimum viable product phase, reinforcing that legacy rails are evolving alongside stablecoins rather than being displaced.

PayPal: The Interface Layer

PayPal’s expansion into 70 global markets reflects the evolution of the user experience layer. Its multi-coin strategy allows users to hold and transact across multiple stablecoins within a single interface.

This simplifies blockchain-based finance into familiar digital payment experiences. Cross-border transfers that once required specialized knowledge now resemble standard app-based transactions.

This visible, wallet-driven approach contrasts with a parallel trend where stablecoins operate as invisible infrastructure behind existing systems.

The Invisible Rail: Visa and Stripe

Visa and Stripe are embedding stablecoins directly into backend systems. Users continue to transact through familiar methods, while stablecoins handle settlement in the background.

Stripe’s acquisition of Bridge is enabling automated and programmable payments, particularly in emerging areas such as AI-driven commerce.

AI agents are beginning to pay for APIs, compute, and data in real time. These machine-to-machine transactions require instant, low-cost, and globally interoperable settlement, positioning stablecoins as a natural fit.

Beyond Payments: Tokenized Finance Expands

Stablecoins are increasingly serving as the entry point into a broader ecosystem of tokenized assets, including Treasuries and private credit.

Regulators are beginning to support this shift. The U.S. Securities and Exchange Commission is advancing frameworks for tokenized securities and on-chain settlement, while the International Monetary Fund has warned that these systems could introduce new forms of systemic risk.

Recent developments highlight the pace of adoption. SWIFT is building a shared ledger with more than 30 global banks, targeting tokenized deposit settlement by 2026. Major institutions including Barclays, HSBC, Lloyds, and Standard Chartered are advancing similar initiatives.

At the same time, new payment models are emerging. Stablecoins are being integrated into machine-driven transactions, with protocols designed for AI agents to pay for services such as compute and data in real time.

Market data reinforces the trend. Stablecoin supply reached approximately $315 billion in early 2026, with transaction volumes now rivaling traditional payment networks.

The Verdict: Enterprise Utility Is the New Normal

Stablecoins have entered a phase defined by integration and enterprise adoption. What began as a yield-driven use case is now focused on efficiency, interoperability, and real-world utility.

Major players across payments and banking are incorporating stablecoins into core operations, while new forms of digital money compete for dominance in settlement.

The RWA payments shift reflects a broader transformation in financial infrastructure. Stablecoins are not only improving how money moves today but are also enabling new forms of economic activity, including programmable finance and machine-driven transactions.

In 2026, the narrative is no longer about experimentation. It is about execution.

Disclosures: This article is for informational purposes only and should not be considered financial, legal, tax, or investment advice. It provides general information on cryptocurrency without accounting for individual circumstances. Sarson Funds, Inc. does not offer legal, tax, or accounting advice. Readers should consult qualified professionals before making any financial decisions. Cryptocurrency investments are volatile and carry significant risk, including potential loss of principal. Past performance is not indicative of future results. The views expressed are those of the author and do not necessarily reflect those of Sarson Funds, Inc. By using this information, you agree that Sarson Funds, Inc. is not liable for any losses or damages resulting from its use.